Introduction

Defining rules of credit during the contracting / planning stages is one of the most important steps for effective monitoring and controlling based on ‘S’ curves and Earned Value Management. Without proper definition of rules of credit measuring planned value of work and earned value of work is not possible.

Rules of credit are used to measure the progress of work completed against the planned work. The most commonly used rules of credit are;

- 0/100 – Work is considered as earned (completed) when it is 100% completed.

- 50/50 – 50% of the work is considered as earned as soon as the work starts. The remaining 50% will be considered as earned only when the remaining 50% is fully completed.

- 25/75 – 25% of the work is considered as earned as soon as the work starts. The remaining 75% is considered as completed only when 100% of the work is completed.

- 20/80 – 20% of the work is considered as earned as soon as the work starts. The remaining 80% is considered as completed only when 100% of the work is completed.

- When none is defined, we apply % completed based on actual measurement or expert judgment.

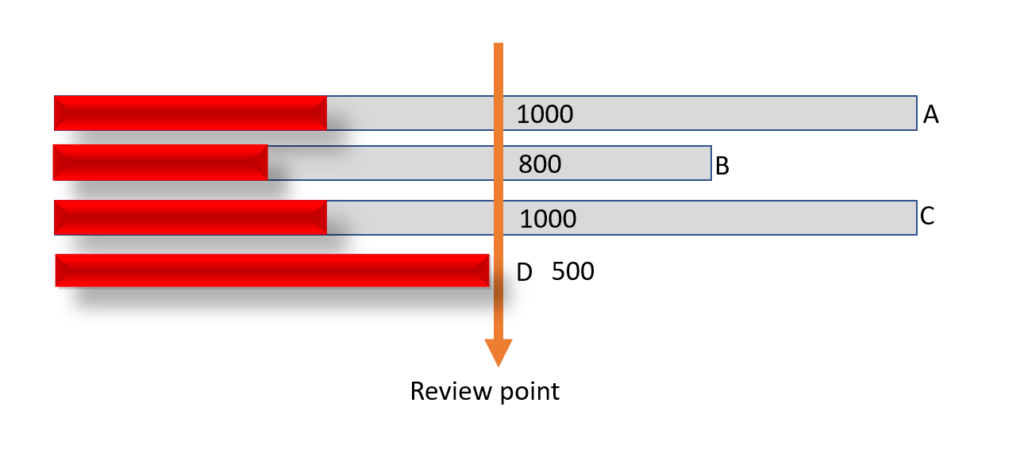

Rules of Credit – Examples

Let us see how the progress is reported based on the various rules of credits discussed above. The orange arrow indicates the review point.

0-100

| Activity | Earned Value |

| A | 0 |

| B | 0 |

| C | 0 |

| D | 500 |

| Total | 500 |

50-50

| Activity | Earned Value |

| A | 500 |

| B | 400 |

| C | 500 |

| D | 500 |

| Total | 1900 |

Summary

Defining rules of credit at the activity level during project planning is key to progress monitoring and control. This helps to roll up the project progress information in the activity, work package, milestone, project sequence. The commonly used rules of credit are 0/100, 50/50, 25/75, 20/80 and percentage completion based on actual progress made.